📖 TABLE OF CONTENT 📖

- 1. Challenges in accessing green finance for businesses

- 1.1 The green finance market paradox

- 1.2 Root cause of the crisis

- 1.2.1 High costs, long timelines, and major risks

- 1.2.2 The standards maze

- 1.2.3 Structural barriers facing SMEs

- 2. Green Fintech: Unlocking billion-dollar capital for businesses

- 3. How is green fintech solving the green finance puzzle for businesses?

- 3.1 Enhancing capital access through smart financing

- 3.2 Strengthening ESG management capabilities through Data technology

- 4. Conclusion

As ESG standards increasingly become the "entry ticket" to global markets, green finance is emerging as a major advantage for many businesses. Instead of getting stuck in legal barriers, complex procedures, and traditional credit profiles, Green FinTech is paving a new track one where businesses can accelerate access to capital, automate sustainable governance, and build transparency into every ESG data stream.

The question is no longer “Should we?”, but rather: Is your business ready to get on board?

1. Challenges in accessing green finance for businesses

1.1 The green finance market paradox

A troubling paradox is unfolding in the global green finance market. While the demand for green transition investment is surging with market projections reaching USD 23 trillion by 2030 and the green bond market alone expected to hit USD 5 trillion by 2025, businesses are facing major systemic barriers that hinder access to capital.

Data from the Organisation for Economic Co-operation and Development (OECD) reveals that up to USD 120 trillion is sitting idle across private investment funds, banks, and individual investors an enormous pool of resources that remains largely untapped for the green transition.

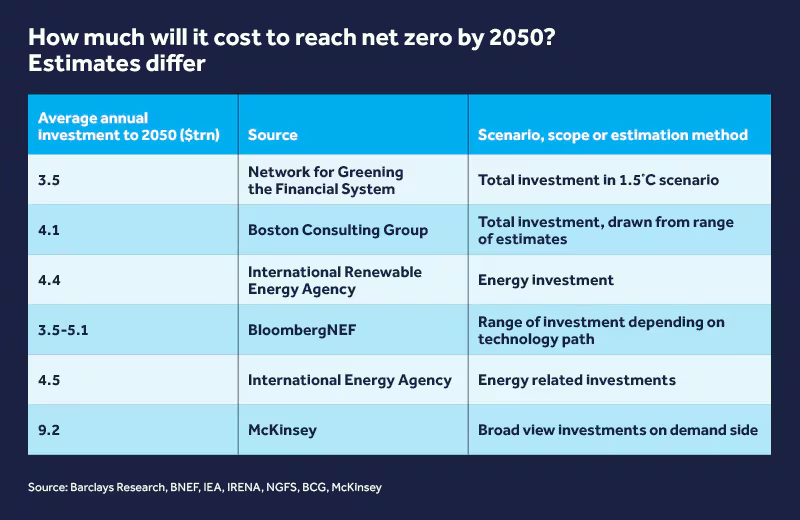

How much will it cost to achieve net-zero emissions by 2050? (Source: Internet)

The core issue is not a lack of capital but rather that capital is flowing in the wrong direction. Each year, nearly USD 7 trillion continues to be funneled into activities that directly harm nature, from both public and private sectors. This figure represents around 7% of global assets and is over 30 times higher than the approximately USD 200 billion invested in green solutions in 2022.

This misalignment reveals a harsh reality: while businesses are actively seeking green financing, the financial system still lacks effective mechanisms to connect capital supply with demand. This is not merely a market inefficiency it poses an existential challenge for businesses striving to go green.

1.2 Root cause of the crisis

1.2.1 High costs, long timelines, and major risks

Statistics show that sustainable infrastructure projects often exceed estimated costs by an average of 80% and face delays of around 20 months compared to original schedules. These characteristics make such projects appear as high-risk or slow-return investments in the eyes of financiers.

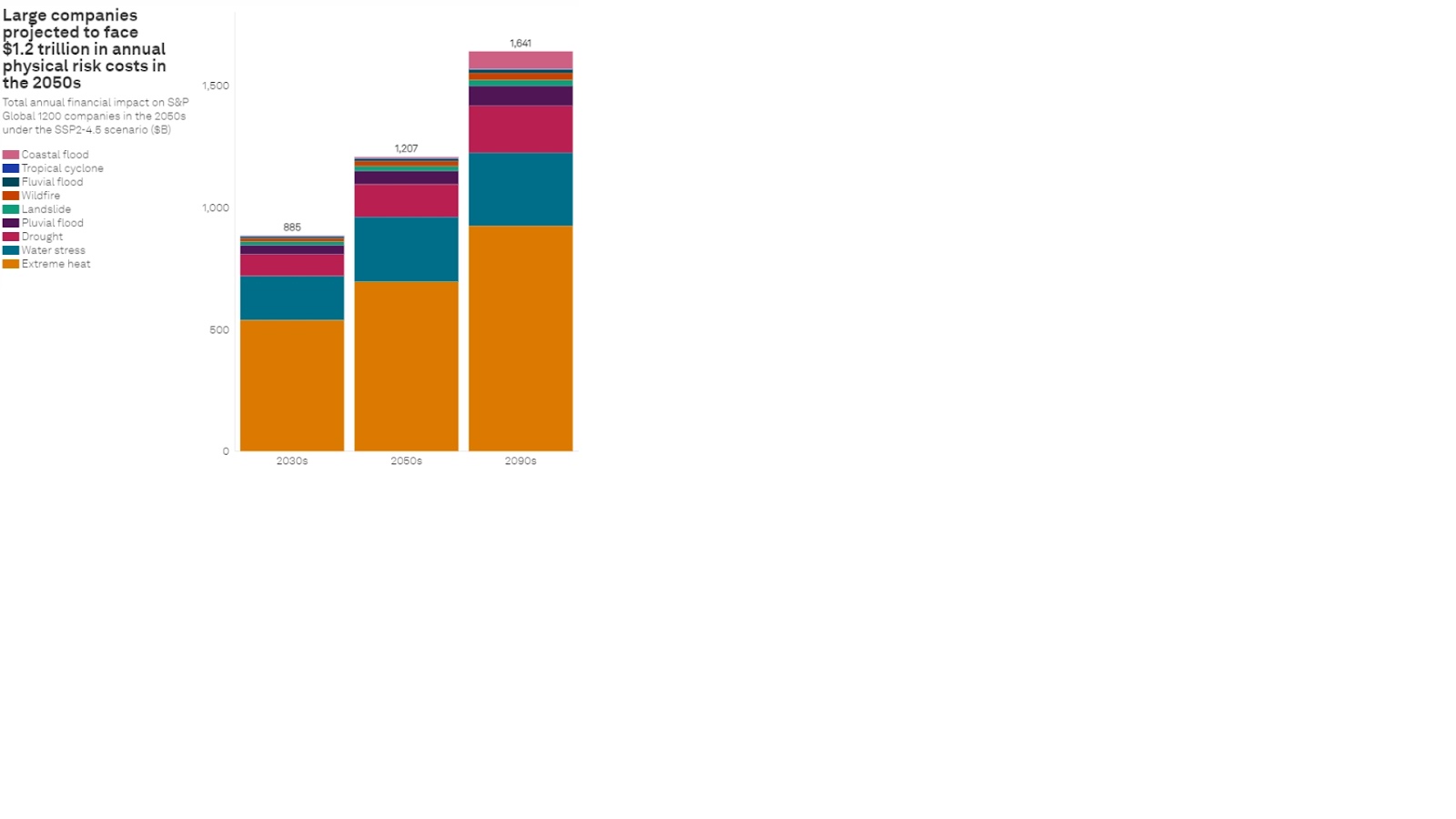

An even more alarming paradox lies in risk perception. While the impacts of climate risks projected to cost up to USD 1.2 trillion per year by 2050 for major corporations alone are often underestimated, the risks of proactive green investments are frequently exaggerated.

This bias creates a vicious cycle: businesses struggle to convince investors, resulting in a limited number of green projects, and ultimately, a stagnation of the entire green finance ecosystem.

Financial implications of climate risks for major companies (Source: Internet)

1.2.2 The standards maze

One of the biggest challenges today is the lack of harmonization in ESG (Environmental, Social, and Governance) reporting frameworks. A variety of standards such as GRI, SASB, TCFD, and CSRD coexist in the market, leading to fragmentation in how businesses collect and disclose ESG data.

This lack of standardization makes it difficult for investors to compare, assess, and make informed capital allocation decisions. Unlike financial metrics, which are governed by well-established accounting standards, ESG data tends to be qualitative and lacks consistent measurement tools reducing its reliability, comparability, and verifiability.

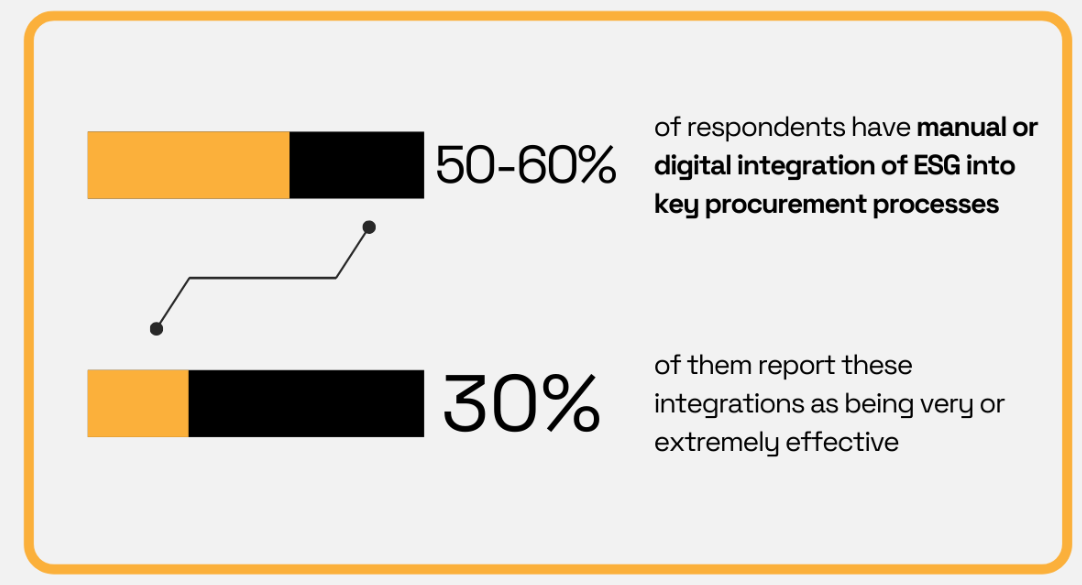

Level of ESG integration (Source: Internet)

Moreover, many businesses still rely on manual methods to collect and manage ESG data, resulting in errors, lack of transparency, and the inability to conduct independent audits. This raises serious concerns about greenwashing where ESG disclosures serve more as publicity tools than as genuine reflections of sustainable performance.

Regulators and central banks have warned that unless ESG data becomes more consistent and transparent, the financial system will struggle to accurately assess climate-related and sustainability risks. This lack of trust may further discourage investors, causing capital flows into green initiatives to remain sluggish.

1.2.3 Structural barriers facing SMEs

Small and medium-sized enterprises (SMEs) play a critical role in the global economy, contributing significantly to GDP and accounting for up to 70% of global environmental pollution. Yet, they face numerous fundamental and systemic barriers in transitioning to sustainable development.

First, many SMEs lack sufficient awareness and understanding of environmental sustainability at all levels ownership, management, and staff. With smaller workforces, limited technical expertise, and tight financial resources, SMEs often struggle to implement environmental initiatives effectively. Many business owners remain skeptical, fearing that sustainability efforts require high upfront costs and long payback periods. As a result, they tend to prioritize cost-cutting and short-term survival over long-term environmental goals.

Challenges faced by small and medium-sized enterprises (SMEs) in accessing green finance (Source: Internet)

The second major challenge is the dual financial barrier. SMEs not only face difficulties in accessing traditional credit due to complex procedures, long processing times, and high interest rates but also lack access to green financial products specifically tailored to their scale and characteristics.

If SMEs key contributors to environmental pollution are not supported in the green transition, global environmental targets will be severely compromised, regardless of efforts made by large corporations. Addressing the challenges faced by SMEs is therefore not just a matter of financial inclusion, but a strategic imperative to achieve comprehensive and sustainable green growth.

2. Green Fintech: Unlocking billion-dollar capital for businesses

As traditional financial models struggle to keep pace with the demands of the modern era, businesses must adopt a more innovative lens to adapt.

This is where Green Fintech the groundbreaking fusion of financial technology and environmental innovation emerges as a key enabler. It shortens the distance between capital and businesses, drives the financial sector toward sustainability, enhances brand reputation, and contributes to the United Nations’ Sustainable Development Goals (SDGs).

Unlike the broader concept of sustainable finance, which integrates Environmental, Social, and Governance (ESG) factors, Green Fintech focuses exclusively on environmental objectives. At its core, Green Fintech is dedicated to developing financial solutions that support carbon footprint reduction, energy efficiency, and renewable energy projects.

It is not merely an auxiliary tech stream but rather a fundamental transformation in how the financial system operates to serve environmental and sustainable development goals.

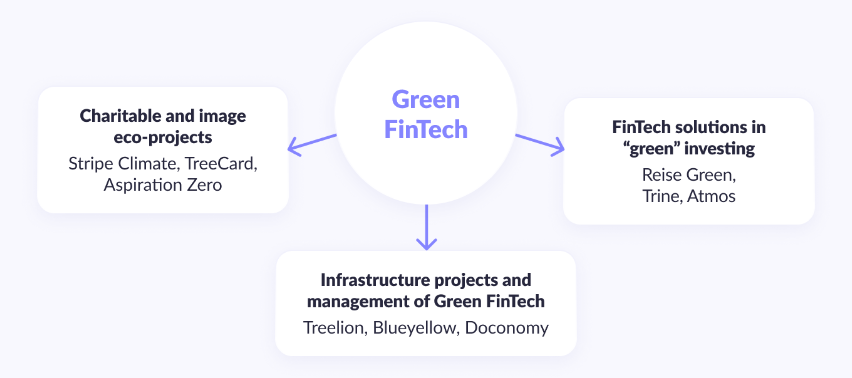

Green Fintech ecosystem (Source: Internet)

Green Fintech applications today are highly diverse ranging from green digital payments, environmental risk analytics using big data, and green crowdfunding, to green digital assets, environmental management technologies, and more. What these solutions share is their potential to revolutionize how finance operates: faster, more accurate, and more environmentally friendly.

To fully understand the role of Green Fintech within the broader sustainable finance landscape, it's essential to distinguish the two concepts clearly:

Green Fintech focuses on technological innovations and solutions aimed specifically at achieving environmental objectives. In contrast, Sustainable Finance encompasses a broader scope, integrating Environmental, Social, and Governance (ESG) factors into the entire financial decision-making process. In this sense, Green Fintech can be viewed as a specialized branch of sustainable finance, with a concentrated focus on environmental issues.

As a catalyst for sustainable development, Green Fintech is powerfully unlocking green capital for businesses through several key drivers:

1. Building a Dynamic Green Finance Ecosystem

Green Fintech is shaping a more environmentally conscious financial environment, supporting the achievement of the Sustainable Development Goals (SDGs) while creating new investment opportunities for both businesses and responsible investors.

2. Optimizing Capital Allocation into Green Projects

By leveraging technologies such as AI, blockchain, and big data, fintech solutions can accurately assess risk levels, return potential, and environmental impact of individual investments thereby enabling more efficient capital flows into green initiatives

3. Expanding Access to Green Finance

Digital platforms help overcome traditional financing barriers such as complex paperwork, lack of collateral, or geographic limitations thus enabling SMEs and vulnerable groups to access green capital more easily.

4. Reducing Emissions in Financial Operations

Green Fintech enables the full digitization of financial processes from payments and lending to investment product issuance. This not only improves operational efficiency but also significantly reduces emissions from activities like printing, paper-based transactions, and physical travel.

Today, the future of finance lies not just in profit growth, but in the ability to create sustainable value for society and the environment. Against this backdrop, Green Fintech is emerging as a strategic driver, helping businesses overcome traditional financial barriers, accelerate innovation, and restructure growth models toward green transformation.

3. How is green fintech solving the green finance puzzle for businesses?

3.1 Enhancing capital access through smart financing

a. Digitizing financial processes - The first step toward efficient capital access

One of the greatest challenges for businesses pursuing green initiatives is the complexity of financial and regulatory processes. Green Fintech is addressing this barrier by digitizing and automating the entire financial workflow from identity verification to loan approval and disbursement.

A prominent trend in this area is RegTech (Regulatory Technology) a technology that automates auditing and compliance procedures. With RegTech, businesses can save up to 60% of the time, 40% of audit costs, and reduce compliance costs by up to 30%, thereby boosting operational efficiency in a landscape of increasingly strict regulations.

RegTech typically operates through four key steps:

-

Objective: Customer Onboarding: Automates the process of customer authentication and verification, helping to detect fraud and prevent potential threats.

-

Responsibility: Continuous Monitoring: Utilizes cloud computing and big data methods to manage consumer data streams efficiently, ensuring real-time compliance monitoring.

-

Problem to Solve: Detection of Suspicious Transactions: Analyzes transactions and activities to identify recurring patterns or “red flags” that indicate regulatory violations. Machine learning algorithms are used to accurately flag these patterns.

-

Timeline: Comprehensive Reporting: Gathers complete information on suspicious activities and reports violations to regulators. This step is mandatory to maintain regulatory integrity.

Definition of RegTech (Source: Internet)

Not only that, the adoption of digital signatures, electronic payments, and digital document management platforms also helps reduce the carbon footprint of financial operations making these technologies well-aligned with the green development goals of many businesses today.

b. Optimizing Green Capital Mobilization through Green Bonds and Sustainability-Linked Loans

For small and medium-sized enterprises (SMEs) or green startups, accessing capital often proves difficult due to a lack of collateral or limited credit history.

Green Fintech has opened new avenues through alternative credit models such as peer-to-peer (P2P) lending, using AI algorithms and non-traditional data including utility bill payments, digital transactions, and internet usage behavior to assess creditworthiness quickly and accurately.

Green Fintech also facilitates access to green capital through financial instruments like green bonds and sustainability-linked loans (SLLs). These instruments are increasingly favored by environmentally committed investors, creating new fundraising channels for eco-friendly projects.

Among these, green bonds are debt instruments issued to finance projects with a positive environmental impact, such as renewable energy, energy efficiency improvements, waste management, and green transportation. Fintech plays a key role in streamlining the issuance process and enhancing transparency in green bond transactions.

A notable example is the Path2Zero project the world’s first net-zero emissions ethylene cracker plant. This facility specializes in separating hydrocarbon molecules from petroleum or natural gas to produce ethylene, a key input in the petrochemical industry. Remarkably, the bond issuance for this project attracted over 200 investors, including 75 new ones. This demonstrates that green bonds are not only effective financial tools but also highly appealing to the sustainable investor community, helping accelerate the global advancement of green finance.

Issuance and operational process of Green Bonds (Source: Internet)

In addition, Sustainability-Linked Loans (SLLs) are a form of financing that does not require the borrowed capital to be used for a specific green project. Instead, the interest rate is adjusted based on whether the borrower meets its pre-agreed ESG targets. This represents a strategic evolution in green finance shifting the focus from “use of proceeds” to the overall ESG performance of the business.

Compared to traditional green bonds or green loans, SLLs offer greater flexibility, allowing businesses to use the funds for general operations, as long as they achieve their sustainability commitments.

c. Increasing transparency and creating market incentives through carbon credits

Beyond direct capital access, Green Fintech also plays a critical role in building transparent and efficient carbon credit markets, enabling businesses to turn emissions reduction efforts into tangible economic benefits.

Fintech platforms such as Carbonplace and Carbon Trade Exchange (CTX) are providing the digital infrastructure for the entire lifecycle of carbon credit trading covering certification, listing, trading, payment, and data storage. By leveraging blockchain and cloud computing, these platforms ensure:

-

Objective: High transparency regarding credit origin, issuing bodies, project types (e.g. afforestation, renewable energy), and measurable environmental impacts.

-

Responsibility: Real-time traceability, enabling businesses to monitor ownership status, transactions, and remaining or utilized credit volumes.

-

Problem to Solve: Automated ESG reporting, with standardized data aligned with international disclosure frameworks.

-

Timeline: (To be determined based on project phases and integration milestones.)

For businesses, this not only helps meet the growing demands of investors and global partners, but also empowers them to design more flexible emission reduction strategies balancing internal efforts with market-based offset mechanisms.

Notably, to enhance transparency in the issuance and use of green finance instruments such as green bonds and SLLs, many Fintech platforms are now integrating blockchain and smart contract technologies.

In the carbon credit market, blockchain helps establish a “single source of truth”, eliminating risks of double-counting, enabling full lifecycle traceability of credits from issuance to retirement, and standardizing data across systems. For example, JPMorgan and S&P Global are jointly piloting the tokenization of carbon credits, aiming to transform the USD 200 billion voluntary carbon market into a transparent, liquid, and investor-friendly ecosystem.

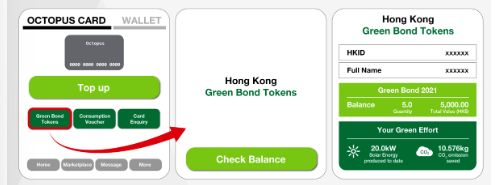

Blockchain has also been applied in green bond issuance. In 2023, the Hong Kong government issued its first tokenized green bond worth HKD 800 million. The issuance was conducted on a private blockchain platform integrated with smart contracts, which digitalized the entire process from issuance and settlement to coupon payment and maturity ensuring real-time transparency and eliminating manual intervention.

Notably, transactions were settled using delivery-versus-payment (DvP) with tokenized cash issued by the Hong Kong Monetary Authority, and all ownership records on the blockchain were legally recognized under Hong Kong law [a]. This was not only a technical breakthrough but also a showcase of the synergy between green finance, digital assets, and progressive legal frameworks, paving the way for more sustainable and transparent issuance models in the future.

Green Bond Management and Verification via Digital Wallet – Source: Internet

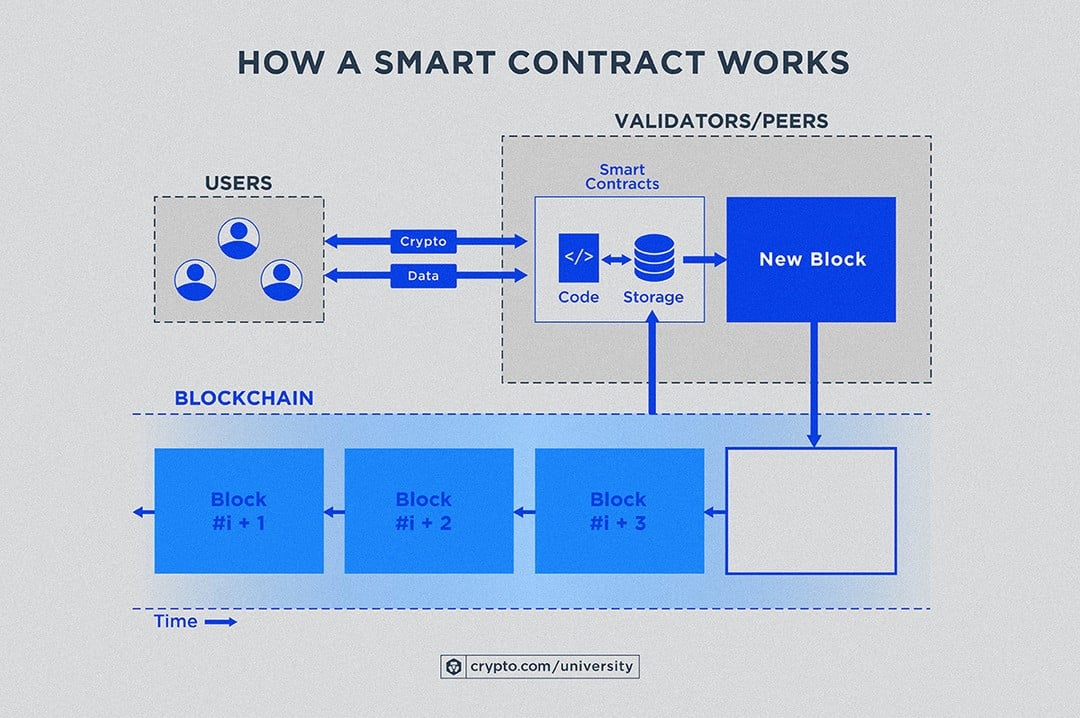

Moreover, smart contracts a key extension of blockchain technology play a crucial role in automating and enforcing commitments in green finance, adding another layer of trust and efficiency to sustainable financial instruments.

How smart contracts work (Source: Internet)

Smart contracts serve as a “digital guarantee mechanism” they are pre-programmed code that runs directly on the blockchain, automatically triggering actions when predefined conditions are met. Unlike traditional contracts, smart contracts eliminate manual intervention entirely, thereby enhancing compliance and minimizing the risk of errors.

Practical benefits include reduced operational costs due to the removal of intermediaries, faster transaction processing, and assurance that all activities are recorded transparently and are auditable. More importantly, this mechanism paves the way for innovative financial models such as Sustainability-Linked Loans (SLLs), where interest rates can be automatically adjusted based on the achievement of ESG targets. This enables businesses to access preferential capital in a fair and responsible manner.

In addition, some Green Fintech solutions are democratizing access to carbon offsetting mechanisms for end consumers especially in the e-commerce sector.

Among them, EcoCart stands out: a platform that helps online retailers integrate carbon offsetting into the checkout process and enables customers to contribute to environmental projects such as reforestation and renewable energy. EcoCart has been adopted by more than 2,000 retail businesses, helping increase average cart conversion rates by 14% and enhancing green brand perception.

3.2 Strengthening ESG management capabilities through Data technology

As sustainable development increasingly becomes a strategic standard, businesses face two major challenges:

(1) ensuring transparency in ESG disclosure, and

(2) managing risks related to climate change, legal regulations, and brand reputation.

Green Fintech, with its modern data technology platforms, enables businesses to proactively manage, forecast, and optimize ESG performance in real time rather than merely reacting to demands from the market or regulators.

a. Expanding ESG Credit Assessment Capabilities with Non-Traditional Data

One of Green Fintech’s breakthrough contributions is its ability to assess companies’ creditworthiness and sustainability performance using non-traditional data, instead of relying solely on financial statements or credit history.

With the support of Artificial Intelligence (AI), fintech platforms can analyze utility bill payments, digital activity, electronic transactions, and even satellite imagery to provide credit assessments for individuals and organizations that have never accessed the formal financial system.

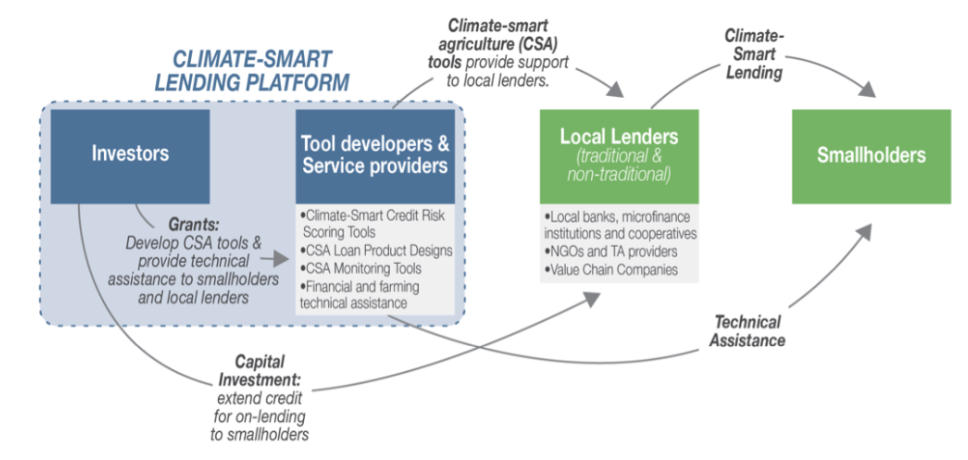

For example, in a pilot agricultural project in Kenya, satellite imagery and AI were used to evaluate the creditworthiness of unbanked farmers. AI analyzed data on crop yields and soil conditions from satellite sources to forecast repayment ability, helping farmers secure loans for climate-smart agriculture. This is a clear case of using environmental data (satellite imagery) to address a financial challenge (credit access) for a sustainable goal (climate-smart agriculture).

Climate-based smart lending platform (Source: Internet)

b. Automating ESG Data Collection, Analysis, and Standardization

Green Fintech not only assists in credit assessment but also streamlines the ESG management process a process traditionally labor-intensive and prone to errors when handled manually. By leveraging the integration of AI, Big Data, IoT, and Natural Language Processing (NLP), businesses can:

-

Objective: Automatically extract ESG-related information from various sources such as sustainability reports, financial statements, invoices, IoT data, or satellite images — eliminating manual tasks, reducing errors, and accelerating processing speeds.

-

Responsibility: Analyze unstructured data such as legal reports and internal documents using LLMs (Large Language Models) and NLP to detect potential ESG risks, track carbon footprints, and identify bottlenecks in sustainability performance.

-

Problem to Solve: Standardize and consolidate data from various systems, breaking down information silos and creating a centralized, auditable ESG data source that is accessible and efficiently reportable.

-

Timeline: (To be defined based on integration and system rollout phases.)

Thanks to this, businesses can not only ensure compliance with increasingly strict ESG regulations, but also make real-time, data-driven decisions at lower costs.

How AI is transforming the FinTech industry (Source: Internet)

c. Proactively Forecasting and Mitigating ESG Risks

In addition to ensuring transparency and efficiency in ESG governance, Green Fintech also provides specialized risk forecasting models, enabling businesses to proactively manage the impacts of climate change and non-financial risks.

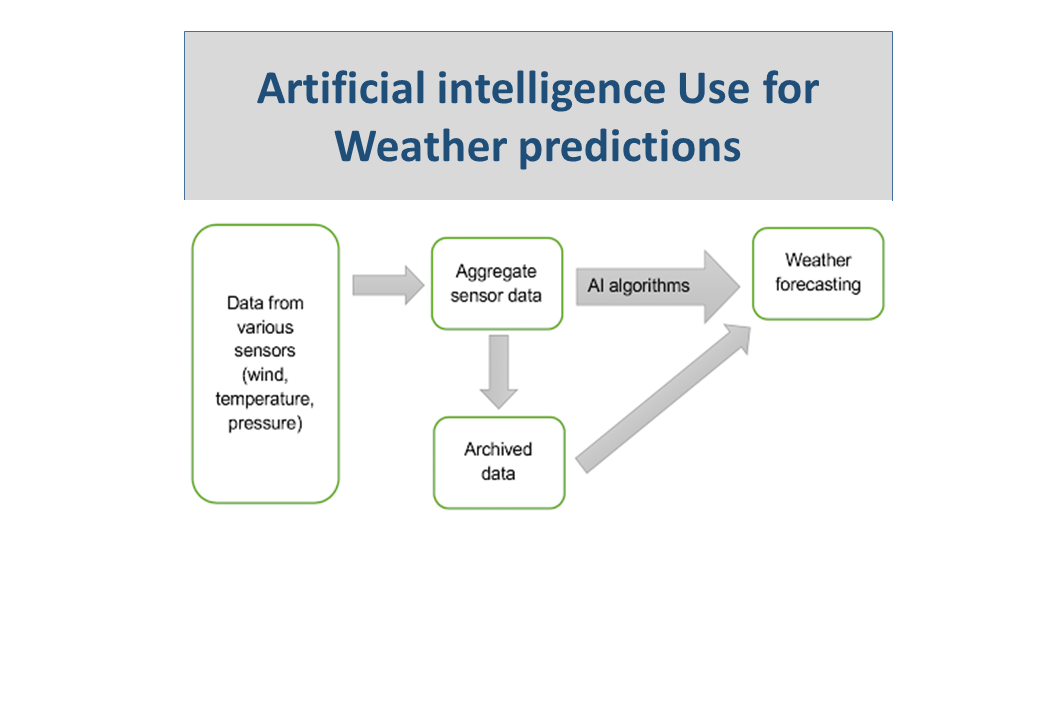

AI is now being applied across various domains such as predicting the vulnerability of investment portfolios to extreme weather events, assessing carbon transition risks, monitoring the environmental performance of green loans, and optimizing real-time resource usage to reduce costs and waste.

A standout example is Arbol a company that offers weather risk insurance products for events such as droughts, floods, and temperature fluctuations, serving farmers and enterprises worldwide. In India, Arbol partnered with agricultural businesses to deploy rainfall-based insurance. When rainfall levels recorded at weather stations fall below a predetermined threshold, the system automatically triggers payouts without requiring farmers to file claims or wait for loss assessments ensuring timely and transparent support.

Data flows and AI applications in weather forecasting (Source: Internet)

4. Conclusion

Green Fintech is more than just a financial tool it is a technological solution to the challenge of sustainable development. In a world where environmental risks are increasingly becoming financial risks, integrating technology into every link of the financial system is no longer optional it is essential.

From customer identification to alternative credit assessment, from ESG transparency to crowd-based fundraising, Green Fintech is rewriting how capital is created, circulated, and allocated.

Ecosystem of green and sustainable finance solutions (Source: Internet)

More importantly, Green FinTech opens the door for businesses especially SMEs to embark on the green transition not through pressure, but through opportunity. When every financial transaction can reflect a positive environmental footprint, finance evolves from being a tool for growth to becoming a compass for a sustainable future.

BambuUP brings together a comprehensive network of experts, partners, and solutions, ready to support manufacturers, industrial zones, and factories on their green transformation journey from optimizing production operations to enhancing export capacity and brand value in global markets.

We have proudly partnered with leading corporations across diverse industries such as Shinhan, EVN, Heineken Vietnam, FASLINK, DKSH Smollan, and others in launching open innovation challenges. As a trusted strategic partner, BambuUP is committed to empowering businesses in their innovation efforts and driving bold green transitions.

To stay updated with the latest insights on Innovation and Green Transformation in Vietnam, you can: